Your child says, “I want to study abroad.”

You feel pride. And then the biggest question arises.

Is it worth ₹40 lakhs? ₹60 lakhs? ₹1 crore?

Should we break savings? Take a loan? Do both?

What if the rupee weakens?

What if the job market slows?

The questions are endless, the mind is flowing with infinite thoughts looking for answers.

If you searched for a parent guide to study abroad funding, you are not looking for inspiration. You’re looking for a structure.

And you’re not alone.

According to the Ministry of Education, more than 1.8 million Indian students are studying abroad, and every year over 7.5 lakh students leave India for higher education. Source

As more students go overseas, education loans have also increased. Public banks, private banks, and NBFCs are lending more to support the study abroad plans.

That tells us something important.

Indian families are not just dreaming globally. They are financing globally.

This comprehensive parent guide to study abroad funding walks you from basics to advanced planning. From destination selection to education loan vs savings, from ROI calculations to currency risk management. We’ll cover the financial, emotional, and strategic layers, so you don’t just send your child abroad, but you also fund it wisely.

How to Choose the Right Country and Course for Studying Abroad

Before you calculate EMIs, make sure the country and course actually make sense for your child’s future. The degree should justify the money, time, and effort your family is about to invest.

Start Early: The 12-Month Planning Framework

Admissions in the United States, United Kingdom, Germany, Canada and Ireland are increasingly competitive.

Ideal timeline:

- Start planning 10–12 months before intake

- Shortlist universities 8 months before

- Begin exams and paperwork 6 months before

- Finalize your funding plan 4 months before

Late planning reduces scholarship access and compresses funding decisions.

Overseas education isn’t just an academic choice, it’s a financial investment that needs strategic planning years in advance, notes a financial planning expert in The Economic Times

Comparing Study Abroad Costs vs Salary

Parents often ask the right question: Will this investment recover?

Here’s a simplified snapshot:

| Country | Avg Tuition (₹/year) | Avg Starting Salary (₹ equivalent/year) |

| USA | 30–45 lakhs | 55–75 lakhs |

| UK | 22–35 lakhs | 35–50 lakhs |

| Germany | 0–5 lakhs (public) | 35–55 lakhs |

| Canada | 18–30 lakhs | 30–45 lakhs |

| Ireland | 15–28 lakhs | 40–55 lakhs |

Source: https://www.credila.com/study-abroad/cost-of-studying-abroad

Germany and Ireland are gaining traction because public universities in Germany have minimal tuition fees, while Ireland offers strong tech hiring pipelines.

We break down destination trends, employability outlook, and country-wise opportunities in detail in our guide: https://edufundabroad.in/blog/explore-the-best-places-to-study-overseas/

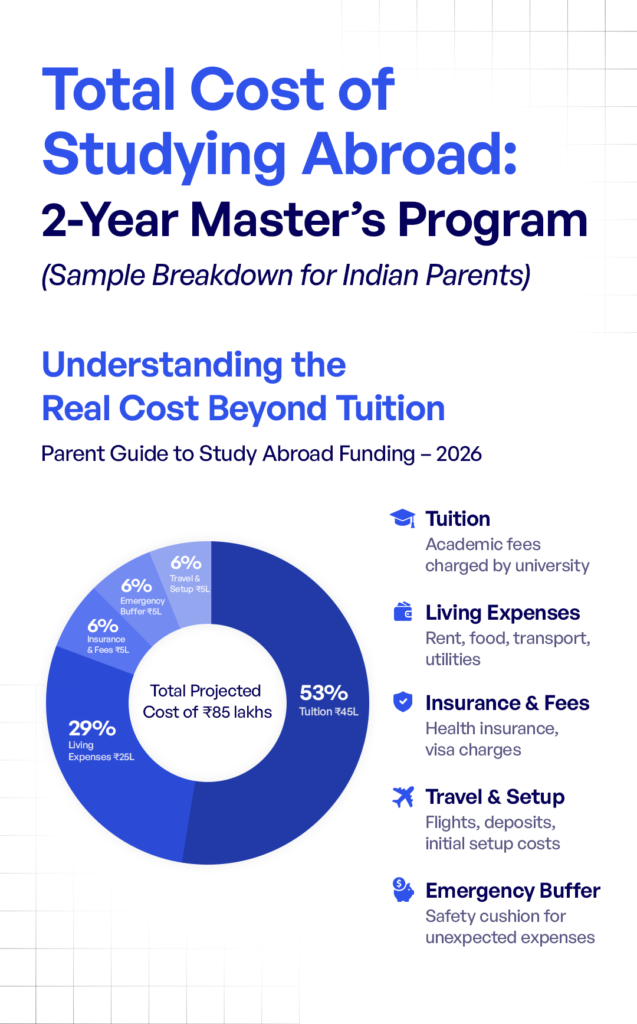

Total Cost of Studying Abroad – The Real Financial Picture

This is where most parent concerns surface. Tuition is only half the story.

Full Cost Breakdown

(2-Year Example: MS in Computer Science, USA)

- Tuition: ₹45L

- Living: ₹25L

- Insurance & Fees: ₹5L

- Travel & Setup: ₹5L

- Emergency Buffer: ₹5L

Total: ₹85L

What this really means is that tuition is just one part of the equation. When you factor in living costs, insurance, travel, and a sensible emergency buffer, the total investment becomes significantly higher than most families initially estimate. Add currency fluctuations into the mix, and the final outflow can shift even further. Early financial planning isn’t about fear, it’s about clarity and control.

Should You Take an Education Loan or Use Savings to Study Abroad?

This is the most searched section within any parent guide to study abroad funding.

Let’s break it down calmly.

Option 1: Fully Funding Through Savings

Pros

- No interest

- No EMI

- Emotional comfort

Cons

- Retirement corpus impact

- Liquidity drained

- Concentrated financial risk

A Delhi-based family funded an MBA entirely from savings. Two years later, a medical emergency forced asset liquidation.

Their views on this: “Liquidity is peace of mind. We underestimated that.”

Option 2: Education Loan

Interest rates range between 9 to 13% depending on lender type.

Benefits:

- Capital preservation

- Tax deduction under Section 80E

- Credit history building

“An education loan is structured leverage when aligned with employability”

Understanding Education Loans in Detail

Many parents hesitate to take loans because they don’t fully understand how banks decide who qualifies and on what terms. Let’s simplify it.

Secured Loans

- Lower interest rates

- Require collateral

- Higher approval threshold

Secured loans usually come with lower interest rates because they’re backed by collaterals such as property or fixed assets. The approval process can be stricter, but if you qualify, the cost of borrowing is generally lower over time.

Unsecured Loans

- No collateral

- Higher interest

- Strong university and course screening

Unsecured loans don’t require collateral, which makes them accessible for many families. However, interest rates are typically higher, and lenders closely evaluate the student’s university, course, and future earning potential before approving the loan.

Lenders evaluate employability, not just admission letters. This is why course choice directly affects loan approval terms.

How Course Choice Affects Study Abroad ROI and Financial Risk

Fields like STEM, AI, data science, engineering, and healthcare typically offer stronger starting salaries and better long-term growth compared to many non-technical degrees. That doesn’t mean other fields aren’t valuable, but from a financial planning perspective, career outcomes matter.

When evaluating a course, parents should look beyond rankings and focus on practical outcomes. What percentage of graduates find jobs within six months? What is the median starting salary? Are there post-study work rights in that country? Is the degree aligned with current industry demand?

Choosing a course with clear employability pathways reduces financial risk and improves return on investment. That’s what strategic funding really looks like.

Questions parents should ask:

- What percentage of graduate’s secure jobs within 6 months?

- What is the median salary?

- What are post-study work rights?

- Is this degree aligned with industry demand?

That’s strategic thinking.

Can Scholarships Fully Cover Study Abroad Costs?

Scholarships can certainly reduce the financial burden, but they rarely eliminate it.

In most cases, they cover 10% to 50% of tuition, and very few fully fund both tuition and living expenses.

Families should assume that housing, food, insurance, and travel will still need to be financed separately.

Government-backed and bilateral scholarship programs do exist, including those facilitated through the Ministry of External Affairs, but they are highly competitive and limited in number. What this really means is simple: treat scholarships as a bonus that lowers your overall cost, not as the primary plan to fund the entire degree.

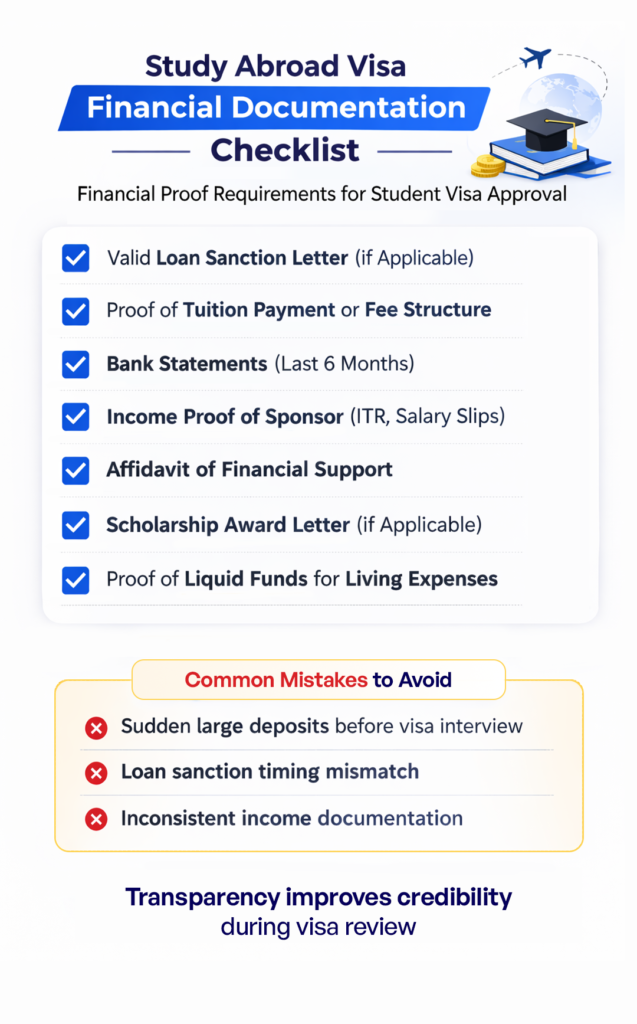

Study Abroad Visa Financial Documents Checklist for Parents

Common mistakes:

- Sudden large deposits before interview

- Loan sanction timing mismatch

- Inconsistent income proof

Visa approvals don’t just depend on admission letters. They depend on clean, consistent financial documentation. Sudden deposits, timing mismatches in loan sanctions, or unclear income proof can raise unnecessary red flags. Clear paperwork builds credibility and reduces last-minute stress.

Preparing Your Child for Financial Independence

Funding alone doesn’t guarantee success.

Students must understand:

- Budgeting

- Rent cycles

- Taxes

- Credit systems

A student in Berlin was spending ₹15,000 monthly on food until he learned basic cooking. His expenses dropped by half and homesickness reduced.

Is Studying Abroad Safe? What Parents Should Plan For

This part is often underestimated. In the beginning, many parents check in constantly, which is completely natural. But as weeks pass, shifting from frequent calls to more structured weekly conversations gives students space to handle small challenges on their own. Support remains strong, just less intrusive, and that space quietly builds confidence and maturity.

Before departure ensure:

- Health insurance active

- Embassy registration

- Digital & physical document copies

- Emergency contacts shared

Study Abroad Cost Planning Checklist for Indian Parents

Before committing:

- Can we sustain 3–4 years financially?

- Have we stress-tested currency risks?

- Are we protecting retirement corpus?

- Is the degree of employability aligned?

- Do we understand loan liability?

If answers are unclear, refine your plan.

Final Thoughts: Funding with Clarity, Not Anxiety

Studying abroad is not just educational spending. It is capital allocation toward human potential. But every investment deserves a structure. The goal of this parent guide to study abroad funding is not to remove risk.

It is to help you understand it.

Structure it. Manage it intelligently.

When funding decisions are deliberate, when education loan vs savings is evaluated carefully, when parent concerns are addressed honestly, stress reduces and opportunity expands.

And when preparation meets ambition, dreams don’t just depart. They land well.

FAQs

1. How much should Indian parents’ budget for studying abroad?

Typically, ₹40L–₹1Cr depends on country and course. Always include living costs and contingency buffers.

2. Is education loan better than using savings?

It depends. Education loan vs savings must be evaluated based on retirement corpus, liquidity needs, and risk tolerance. Hybrid models often work best.

3. What is the ideal emergency fund?

Minimum 6 months of living expenses abroad + 6 months of family expenses in India.

4. How early should funding planning start?

At least 10–12 months before intake.

5. Do scholarships significantly reduce costs?

They help but rarely eliminate the need for structured funding.