Choosing between an education loan vs self-finance for your child’s higher education is as tough as planning for a child’s higher education.

Most parents consider self-financing a viable alternative to pay for their child’s education by liquidating valuable assets like land or FDs or borrowing from family, friends, and relatives.

Such financial assistance is not available to all families. This is when a student loan can help. Let’s look at the benefits of student loans and their preference over self-financing.

Self-financing

Taking out an education loan can be a financial burden for most students and parents, so they prefer self-financing as a viable option to avoid future debt.

For one reason or another, students don’t want to be burdened with EMIs when they can pay for everything at once.

What exactly qualifies as self-financing?

Self-financing may be preferred in the following circumstances:

- Paying for your own education

- Request for financial help from family, friends, or relatives

- Securing funding from a third party (excluding government banks or education loan providers)

Education Loans

In the debate between education loan vs self-finance, education loan has emerged as a strong competitor. The demand for student loans in India has increased steadily even during the pandemic.

Collateral loans or Secured loans are offered based on the collateral provided. When a borrower pledges collateral to obtain a loan, the lender is guaranteed partial compensation for any outstanding loan debt.

In case payments are not made on time, they can seize the mortgage and sell the property. The best mortgage loan providers in India are government and commercial banks

Collateral Free or Unsecured loans do not require any collateral to be pledged. These loans are available to students with insufficient assets to pledge.

However, when financing unsecured loans, lenders consider factors such as parental income, university ranking, and fees are taken into account when considering unsecured loans.

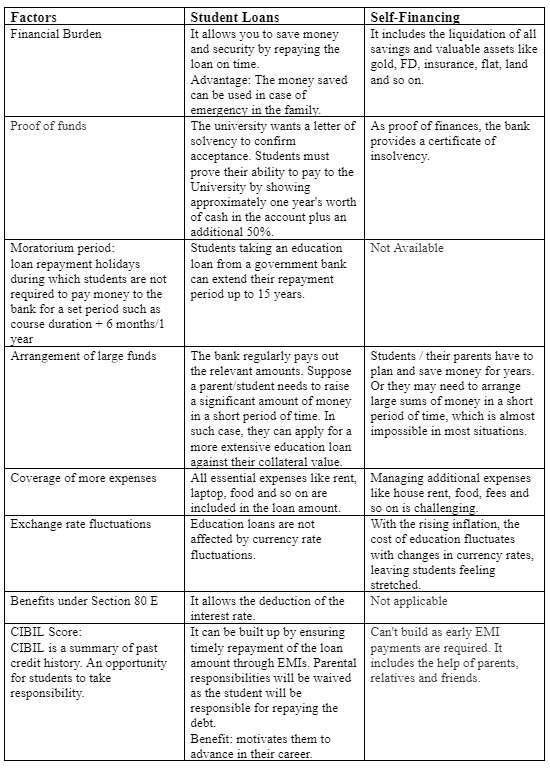

Education loans vs Self Finance

Advice for Students and Parents: Education Loan vs. Self-Finance from EduFund

Deciding between an education loan and self-financing for higher education is a significant choice that can impact a student’s financial future. Here’s a comparative analysis to help students and parents make informed decisions, along with how EduFund can assist in this process.

Education Loan

- Financial Flexibility: Education loans allow students to cover tuition fees, living expenses, and other educational costs without depleting personal savings. This flexibility can help families manage their finances more effectively.

- Lower Interest Rates: Many education loans come with competitive interest rates, especially those offered by government banks. This can make borrowing more affordable compared to other types of loans.

- Deferred Repayment: Most education loans offer a grace period during which students do not need to start repaying the loan until after graduation, allowing them to focus on their studies without financial stress.

- Tax Benefits: Under Section 80E of the Income Tax Act, interest paid on education loans is eligible for tax deductions, providing additional financial relief.

- Building Credit History: Taking out an education loan can help students build a positive credit history if repayments are made on time, which can be beneficial for future financial endeavors.

Self-Finance

- Debt-Free Education: Self-financing allows students to graduate without the burden of debt, providing peace of mind and financial freedom post-graduation.

- Complete Control: Students who self-finance have full control over their finances without the obligations that come with loans, which may lead to greater accountability and responsibility.

- Avoiding Interest Costs: By using personal savings or family contributions, students can avoid interest payments associated with loans, potentially saving money in the long run.

- Immediate Access to Funds: If sufficient funds are available, self-financing allows for immediate payment of tuition and fees without waiting for loan disbursement processes.

Considerations for Decision-Making

- Financial Situation: Assess your current financial status and determine whether you have enough savings to cover educational expenses without compromising your financial stability.

- Long-Term Goals: Consider your career aspirations and whether the potential return on investment from a degree justifies taking on debt through an education loan.

- Risk Tolerance: Evaluate your comfort level with financial risk. Self-financing may seem appealing but could lead to depletion of savings or assets if unexpected expenses arise.

- Future Financial Plans: Think about how either option may affect your future financial commitments or plans for further education.

Conclusion

Student loans come with several benefits, whereas self-funding has limited benefits. Self-funding your child’s higher education can help reduce your child’s financial burden.

Saving for a child’s higher education may be tricky, but if you plan early, you can start from a small amount and create a large corpus over time to protect your child’s future.